Cash Loan vs Personal Loan: Understanding Your Options

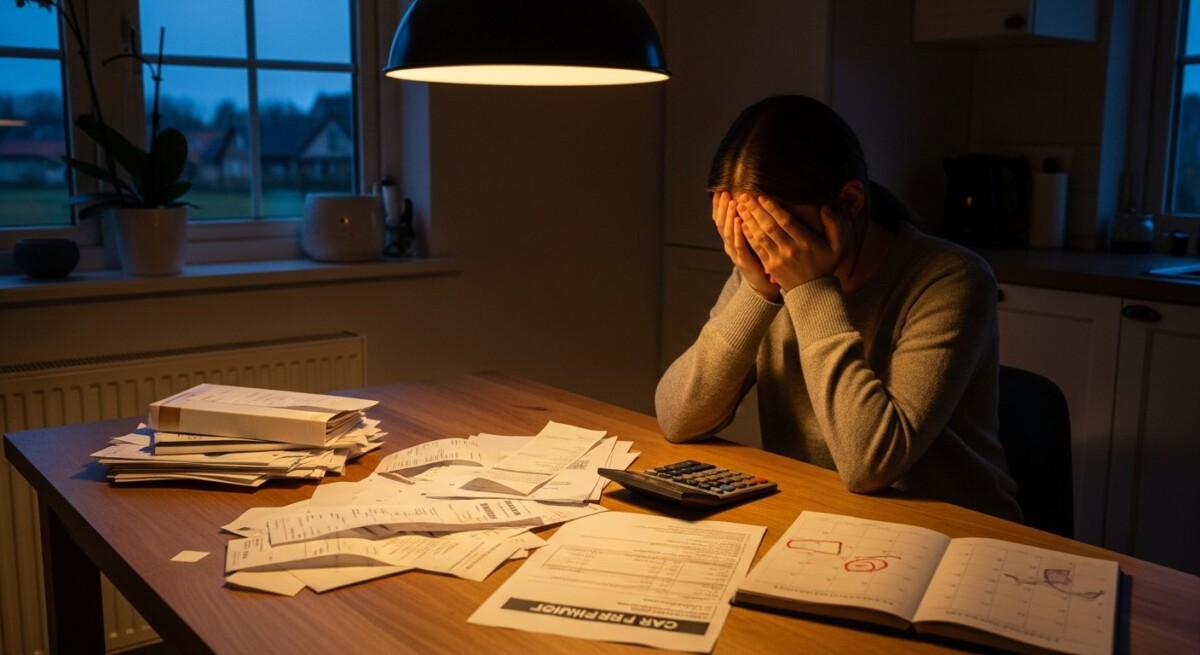

Your car breaks down. An unexpected medical bill arrives. The fridge stops working. Life is full of financial surprises, and when they happen, you need a solution fast. In your search for quick funding, you’ve likely come across terms like “cash loan” and “personal loan.” Understanding the difference between cash loan and personal loan is the first step to finding the right financial help for your urgent situation.

Understanding Difference Between Cash Loan and Personal Loan

At first glance, “cash loan” and “personal loan” might sound like the same thing. Both provide you with money you can use for various needs. However, the key difference lies in the details like speed, amount, and repayment terms.

A cash loan is often a broad term used for short-term, smaller loans designed for immediate cash needs. Think of it as a quick financial band-aid. A personal loan is typically a more formal, longer-term loan for larger amounts, often used for debt consolidation or major purchases.

Knowing which one fits your current need can save you time, stress, and money. It helps you choose a loan that aligns with your ability to repay it comfortably.

What Exactly is a Short-Term Loan?

Since “cash loan” often refers to short-term borrowing, it’s helpful to understand that category. A short-term loan is designed to be repaid quickly, usually within a few weeks to a few months. The application is often fast, with funding possible the same or next day.

When People Consider Short-Term Loans

Short-term loans are considered during times of urgent, unexpected expenses when your regular budget falls short. They are a practical tool for bridging a temporary gap until your next paycheck or until another source of funds becomes available.

These loans are not for long-term financial planning or luxury purchases. They serve a specific purpose: to cover a pressing, necessary cost that can’t wait. Responsible use means having a clear plan for repayment from the start.

Common situations where people explore short-term loans include:

- Unexpected Bills: A high utility bill or a sudden insurance payment.

- Urgent Home or Car Repairs: A leaking roof or a car repair needed for work.

- Medical or Dental Expenses: Costs not fully covered by insurance.

- Temporary Cash Shortages: Covering essentials before a delayed paycheck arrives.

If you are exploring short-term loan options, comparing lenders can help you find the right solution. Request loan offers or call to review available options.

Common Types of Short-Term Loans

When you hear “cash loan,” it might refer to one of several specific loan types. Each has its own structure and is suited for slightly different scenarios. The goal is to match the loan type to your specific financial need and repayment timeline.

Understanding these options helps you ask the right questions and choose wisely. For a deeper dive into how these compare, our guide on payday loans vs personal loans breaks down the specifics.

Here are some common types of short-term funding:

- Payday Loans: Small-dollar loans typically repaid in full on your next payday.

- Short-Term Installment Loans: Loans repaid over a few months in scheduled, regular payments.

- Personal Cash Advances: An advance on your future income or from a credit card.

- Online Line of Credit: A revolving credit limit you can draw from as needed, paying interest only on what you use.

How the Loan Application Process Works

The application process for short-term loans is usually designed for speed. Many lenders offer online applications that can be completed in minutes from your phone or computer. The focus is on verifying your ability to repay the loan quickly.

While requirements vary, the general steps are straightforward. Being prepared with your basic information can make the process even smoother.

A typical application process follows these steps:

- Submit a Request: You provide basic personal, contact, and financial details through an online form or in a store.

- Income Verification: You show proof of steady income, such as recent pay stubs or bank statements.

- Lender Review: The lender reviews your information, which may include a credit check.

- Receive Loan Offers: If approved, you’ll see the exact loan amount, fees, and repayment terms.

- Receive Funds: Upon accepting the offer, funds are often deposited directly into your bank account, sometimes as soon as the same day.

Comparing multiple lenders can help you find loan terms that match your situation. Compare loan offers or call to explore available funding options.

Factors Lenders May Consider

Lenders look at a few key pieces of information to decide on a loan application. Their main concern is your ability to repay the loan on time. This assessment is usually quicker and focuses on different factors than a mortgage or auto loan.

Even if you have less-than-perfect credit, you may still have options, as some lenders prioritize current income. It’s always worth exploring what different lenders require.

Common factors include:

- Proof of Steady Income: Regular paychecks or other reliable income sources.

- Active Checking Account: A bank account in good standing for depositing funds and setting up repayment.

- Employment Status: Current employment or a consistent income stream.

- Credit History: Some lenders may check your credit, while others may not.

Understanding Loan Costs and Terms

This is the most critical part of responsible borrowing. Before accepting any loan, you must understand exactly what it will cost you. The total cost includes the amount you borrow plus all fees and interest charges.

Short-term loans often have fees stated as a fixed dollar amount or a finance charge. Always calculate the total amount you will repay. For a comprehensive look at how costs and structures differ, see our detailed article on cash loan vs personal loan key differences.

Key terms to review are:

- Finance Charge/Fee: The cost to borrow the money.

- Annual Percentage Rate (APR): The yearly cost of the loan, including fees, shown as a percentage.

- Repayment Schedule: The exact dates and amounts of your payments.

- Due Date: The date your full payment is required.

- Late Fees: Charges applied if a payment is missed or late.

Loan terms can vary between lenders. Check available loan offers or call to review possible options.

Tips for Choosing the Right Loan Option

With several options available, taking a moment to compare can lead to a better financial decision. Your goal is to find a solution that solves your immediate problem without creating a larger one down the road.

Think of borrowing as a tool. Used correctly for the right job, it’s helpful. Used without a plan, it can cause damage. Always prioritize loans with clear terms and a repayment plan you can manage.

Follow these practical tips:

- Borrow Only What You Need: Resist the temptation to take extra cash; it means more to repay.

- Compare Multiple Lenders: Look at costs, terms, and funding speed from different companies.

- Read the Agreement Thoroughly: Understand all fees, the due date, and the consequences of a late payment.

- Have a Repayment Plan: Know exactly how you will repay the loan before you accept it.

- Ask Questions: If anything is unclear, contact the lender for clarification.

Responsible Borrowing and Financial Planning

Short-term loans are a financial tool, not a long-term strategy. Using them responsibly means having a clear exit plan,knowing how the loan fits into your budget and when it will be paid off completely.

If you find yourself needing short-term loans frequently, it may be a sign to look at your overall budget. Creating a small emergency savings fund, even just a few hundred dollars, can help you handle future surprises.

The most supportive thing you can do for your financial health is to borrow with intention. Understand the commitment, plan for it, and use the loan to get through a tight spot, not to dig a deeper hole. For more insights on managing different types of credit, our resource on key differences in loan types can be a helpful next read.

FAQs

What is the main difference between a cash loan and a personal loan?

Cash loans are typically smaller, short-term solutions for immediate cash needs, often with quicker funding. Personal loans are usually for larger amounts with longer repayment terms (years) and are often used for planned expenses or debt consolidation.

Can I get a short-term loan with bad credit?

Yes, some lenders offer short-term loans to borrowers with less-than-perfect credit. They may focus more on your current income and employment status rather than your credit score alone.

How fast can I get the money from a short-term loan?

Many online lenders can deposit funds as soon as the same business day or the next business day after approval. In-store applications may provide cash almost immediately.

What happens if I can’t repay my loan on time?

Contact your lender immediately. They may offer an extended payment plan or other options. Be aware that late payments typically result in additional fees and can negatively impact your credit.

Are online lenders safe for short-term loans?

Reputable online lenders use secure encryption technology to protect your data. Always verify the lender is licensed to operate in your state and read reviews from other customers.

What’s the most important thing to look at in a loan agreement?

The total repayment amount. This number tells you exactly how much you will pay back, including all fees and interest. Compare this to the amount you’re borrowing to understand the true cost.

Facing a financial gap can be stressful, but understanding your options puts you in control. By knowing the difference between loan types, comparing offers, and borrowing only what you need with a clear repayment plan, you can navigate urgent expenses confidently. Take your time to review your options carefully and choose the solution that best supports your current situation and future financial well-being.

About Levi Parker

Related Posts