Short Term Cash Loans: A Guide to Fast Funding

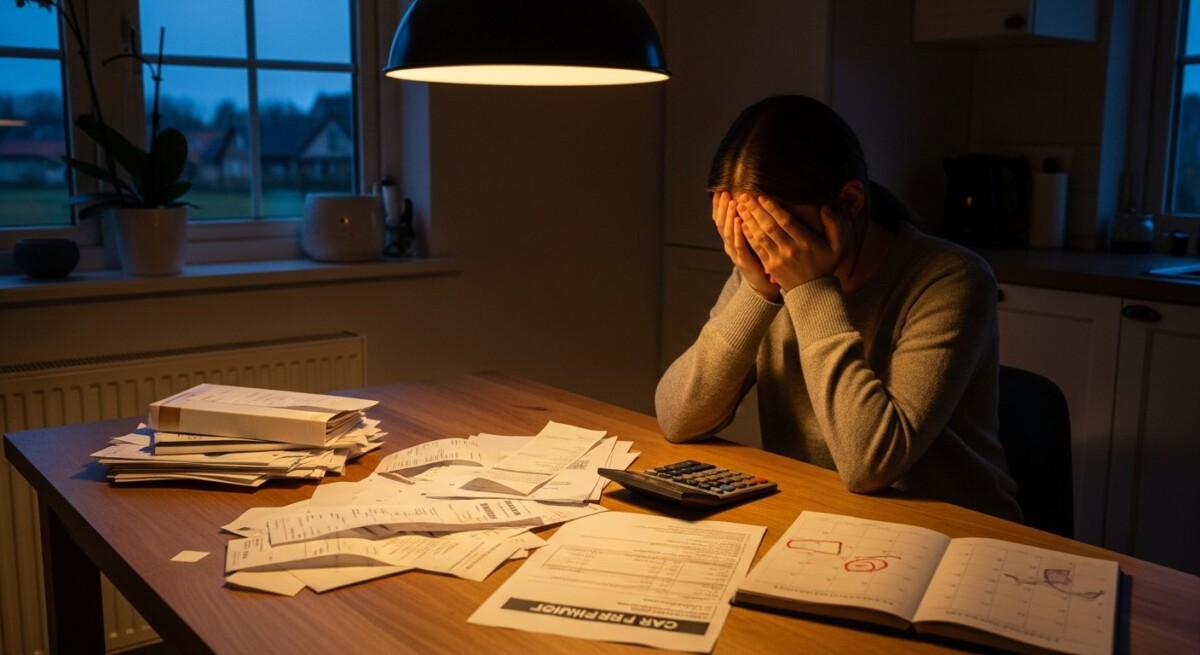

When an unexpected expense arrives before your next paycheck, the financial pressure can feel immediate and overwhelming. A car repair, a medical bill, or a utility shut-off notice doesn’t wait for payday. In these situations, many people consider short term cash loans as a potential solution for quick access to funds. These loans are designed to provide a small, temporary cash advance, typically to be repaid in full on your next payday or within a few weeks. Understanding how they work, their true costs, and the alternatives available is crucial before you commit. This guide will provide a comprehensive look at short term lending, empowering you to make an informed financial decision.

Visit Get Fast Funding to explore your options and make an informed financial decision.

What Are Short Term Cash Loans?

Short term cash loans are a category of small-dollar, high-cost credit intended to bridge a temporary gap in finances. They are generally unsecured, meaning you don’t need to put up collateral like a car or house. The most common types are payday loans and installment loans. A payday loan is usually due in a single lump-sum payment on your next payday, while a short term installment loan allows you to repay the amount borrowed, plus interest and fees, over a series of scheduled payments. The defining characteristics of these products are their speed of funding, often within one business day, and their accessibility to individuals with less-than-perfect credit, as lenders primarily focus on your income and ability to repay quickly.

The application process is typically streamlined, with many lenders offering online applications. Approval can be rapid, sometimes within minutes, with funds deposited directly into your bank account. This convenience, however, comes at a significant cost. The fees and interest rates for short term loans are substantially higher than those for traditional loans or credit cards. It’s vital to look beyond the advertised dollar fee and calculate the Annual Percentage Rate (APR), which annualizes the cost of the loan. An APR for a payday loan can easily reach 400% or more, making it an extremely expensive form of credit.

The Costs and Risks to Consider

Before taking out a short term loan, a clear-eyed assessment of the costs and potential pitfalls is non-negotiable. The primary risk is the debt cycle. Because the loans are due so quickly and the payments can consume a large portion of your paycheck, many borrowers find they cannot cover their other living expenses after repayment. This forces them to take out another loan to get by, a practice known as “rolling over” the loan, which incurs new fees and traps them in a cycle of repeat borrowing. State regulations vary widely, with some capping interest rates and others having more permissive rules, which is why researching local lending laws and options is a critical first step.

Beyond the cycle of debt, there are other financial dangers. If you cannot repay, the lender may initiate collection proceedings, which can damage your credit score and lead to bank overdraft fees if they attempt to withdraw payments from an account with insufficient funds. Some lenders may also offer loan renewals or extensions that add more fees without reducing the principal. To fully understand the commitment, always read the loan agreement carefully. Key questions to answer include the total dollar amount you must repay, the exact due date, the fees for late or missed payments, and what happens if you default.

Evaluating Your True Need

Given the high costs, it’s wise to pause and evaluate if the loan is for a true emergency or a discretionary expense. Ask yourself if the need is urgent and unavoidable (like a critical repair) or if it can be postponed while you explore other options. Create a simple budget to see if you can rearrange funds from other categories to cover the expense. Sometimes, a short term cash loan is sought for bills that could be negotiated, such as setting up a payment plan directly with a doctor or utility company, often without any interest. Exhausting these avenues first can save you hundreds of dollars.

Responsible Borrowing Practices

If, after careful consideration, you decide to proceed with a short term loan, adopting responsible borrowing practices is essential to minimize harm. First, borrow only the absolute minimum amount you need to solve the immediate problem. Do not be tempted to add extra for “cushion,” as this increases your fees and repayment burden. Second, have a concrete, written plan for repayment before you accept the funds. Know exactly which income source you will use to pay the loan back and how you will adjust your spending to ensure that money is available. This foresight is your best defense against the debt cycle.

Third, use only licensed, reputable lenders. Check with your state’s attorney general or financial regulator to verify a lender’s license and review any consumer complaints. Be wary of lenders who do not clearly disclose their fees or who pressure you to act immediately. Finally, treat the loan as a one-time emergency tool, not a recurring part of your financial strategy. Using these loans repeatedly is a clear signal of a budget shortfall that needs a more sustainable solution, such as increasing income or reducing expenses.

Visit Get Fast Funding to explore your options and make an informed financial decision.

Alternatives to Short Term Cash Loans

Fortunately, several alternatives may provide the financial relief you need without the extreme costs of a traditional payday loan. Exploring these options should always be your first course of action.

- Negotiate with Creditors: Contact the company you need to pay (landlord, hospital, auto shop) and explain your situation. Many are willing to set up a payment plan.

- Community Assistance Programs: Local non-profits, religious organizations, and community action agencies may offer grants or no-interest loans for utilities, rent, or medical bills.

- Payment Advance from Employer: Some employers offer payroll advances as an employee benefit. This is essentially an interest-free loan against your earned wages.

- Credit Union Payday Alternative Loans (PALs): Federal credit unions offer these small-dollar loans with APRs capped at 28%, a far cry from triple-digit payday loan rates. Membership is required.

- Pawn Shop Loan: While not ideal, a pawn loan uses an item of value as collateral. If you repay the loan, you get your item back. If not, you lose the item but have no further debt obligation.

Another strategic alternative is to seek out quick approval cash loans from reputable online lenders that may offer more transparent terms and longer repayment periods than storefront payday lenders. The key is to compare the APR and total repayment amount across all available options. Even a high-interest credit card cash advance often has a lower APR than a standard payday loan. Building a small emergency fund over time, even just a few hundred dollars, is the most powerful long-term alternative to break dependence on high-cost borrowing.

Frequently Asked Questions

How fast can I get money from a short term cash loan?

Many online and storefront lenders can deposit funds into your bank account as soon as the next business day, sometimes even on the same day if you apply early and are approved quickly.

Do short term loans require a credit check?

Many payday and short term lenders do not perform a hard credit check with the major bureaus. They primarily verify your income, active checking account, and identification. However, they may check specialized databases that track short term loan usage.

What happens if I can’t repay my loan on time?

Contact your lender immediately. Some may offer an extended payment plan, but this often comes with additional fees. If you default, the account may be sent to collections, impacting your credit score, and the lender may pursue legal action or a bank garnishment, depending on state law.

Are there laws that limit these loans?

Yes, regulations vary dramatically by state. Some states effectively ban high-cost payday lending through interest rate caps, while others permit it with specific rules on loan amounts, fees, and rollovers. It is your responsibility to know your state’s laws.

Can I get a short term loan with bad credit?

Yes, these loans are often marketed to individuals with poor or no credit history. Lenders focus on proof of recurring income more than credit score. This is a core reason for their high cost, as they are taking on more risk. For more insights on navigating this process, our resource on securing fast funding delves deeper into approval criteria.

Short term cash loans are a powerful, yet potentially dangerous, financial tool. They can provide crucial emergency funding when you have no other options, but their high cost and short repayment term make them a last resort, not a first choice. By thoroughly understanding the terms, evaluating all alternatives, and having a solid repayment plan, you can use them cautiously without letting them derail your financial stability. The goal is to solve an immediate cash problem without creating a larger, long-term debt problem.

Visit Get Fast Funding to explore your options and make an informed financial decision.

About David Wheeler

Related Posts